How to read a Balance Sheet

How to read a balance sheet In financial accounting, a balance sheet is a summary compiled by the Accountant of the financial balances of an organization.

In financial accounting, a balance sheet or statement of financial position or statement of financial condition is a summary compiled by the Accountant of the financial balances of an individual or organization, whether it be a sole proprietorship, a business partnership, a corporation, private limited company or other organization such as government or not-for-profit entity. Assets, liabilities, and ownership equity are listed as of a specific date, such as the end of its financial year. A balance sheet is often described as a “snapshot of a company’s financial condition”. Of the four basic financial statements, the balance sheet is the only statement which applies to a single point in time of a business’ calendar year.

Learning how to read a balance sheet starts with looking at its two sides: assets on the left, and financing on the right–which itself has two parts; liabilities and ownership equity. The main categories of assets are usually listed first, and typically in the order of liquidity. Assets are followed by liabilities. The difference between the assets and the liabilities is known as equity or the net assets or the net worth or capital of the company and according to the accounting equation, net worth must equal assets minus liabilities.

As an Accountant in Miami would state, how to read a balance sheet another way to look at the balance sheet equation is that total assets equal liabilities plus owner’s equity. Looking at the equation in this way shows how assets were financed: either by borrowing money (liability) or by using the owner’s money (owner’s or shareholders’ equity). Balance sheets are usually presented with assets in one section and liabilities and net worth in the other section with the two sections “balancing”.

Small business accounting firms that advise clients to operate entirely in cash can measure its profits by withdrawing the entire bank balance at the end of the period, plus any cash in hand. However, many businesses are not paid immediately; they build up inventories of goods and they acquire buildings and equipment. In other words: businesses have assets and so they cannot, even if they want to, immediately turn these into cash at the end of each period. Often, these businesses owe money to suppliers and tax authorities, and the proprietors do not withdraw all their original capital and profits at the end of each period. In other words, businesses also have liabilities.

HOW TO READ A BALANCE SHEET

Accountants in Miami point out that when it comes to understanding business, there are few financial statements more important than the balance sheet. The balance sheet offers critical insight into the health of a business that can be used by:

- Potential investors to decide whether to invest in a company

- Business owners to craft a more effective organizational strategy

- Employees to adjust their processes to better reach shared organizational goals

Whether you’re a business owner, employee, or investor, understanding how to read and understand the information in a balance sheet is an essential financial accounting skill to have.

Here’s everything you need to know about understanding a balance sheet, including what it is, the information it contains, why it’s so important, and the underlying mechanics of how it works.

WHAT IS A BALANCE SHEET?

As Miami accountants, we’re often asked How to read a balance sheet? The balance sheet is a financial document designed to communicate exactly how much a company or organization is worth—its so-called “book value.” The balance sheet achieves this by listing out and tallying up all of a company’s assets, liabilities, and owners’ equity as of a particular date, also known as the “reporting date.”

Typically, a balance sheet will be prepared and distributed on a quarterly or monthly basis, depending on the frequency of reporting as determined by law or company policy.

The Statement of Position

A balance sheet provides a summary of a business at a given point in time. It’s a snapshot of a company’s financial position, as broken down into assets, liabilities, and equity. Balance sheets serve two very different purposes depending on the audience reviewing them.

When a balance sheet is reviewed internally by the accounting and tax department or a business leader, key stakeholder, or employee, it’s designed to give insight into whether a company is succeeding or failing. Based on this information, an internal audience can shift their policies and approach: doubling down on successes, correcting failures, and pivoting toward new opportunities.

When a balance sheet is reviewed externally by a small business CPA or someone interested in a company, it’s designed to give insight into what resources are available to a business and How to read a balance sheet, they were financed. Based on this information, potential investors can decide whether it would be wise to invest in a company. Similarly, it’s possible to leverage the information in a balance sheet to calculate important metrics, such as liquidity, profitability, and debt-to-equity ratio.

External auditors, on the other hand, might use a balance sheet to ensure a company is complying with any reporting laws it’s subject to How to read a balance sheet

It’s important to remember that a balance sheet communicates information as of a specific date. By its very nature, a balance sheet is always based upon past data. While investors and stakeholders may use a balance sheet to predict future performance, past performance is no guarantee of future results.

THE EQUATION

The information found in a balance sheet will most often be organized according to the following equation:

Assets = Liabilities + Owners’ Equity

While this equation is the most common formula for balance sheets, it isn’t the only way of organizing the information. Here are other equations you may encounter:

Owners’ Equity = Assets – Liabilities

Liabilities = Assets – Owners’ Equity

A balance sheet should always balance. Assets must always equal liabilities plus owners’ equity. Owners’ equity must always equal assets minus liabilities. Liabilities must always equal assets minus owners’ equity.

How to read a balance sheet if it doesn’t balance? It’s likely the document was prepared incorrectly. Typically, errors are due to incomplete or missing data, incorrectly entered transactions, errors in currency exchange rates or inventory levels, miscalculations of equity, or miscalculated depreciation or amortization.

Here’s a closer look at what’s typically included in each of those categories of value: assets, liabilities, and owners’ equity.

- Assets

An asset is defined as anything that is owned by a company and holds inherent, quantifiable value. A business could, if necessary, convert an asset into cash through a process known as liquidation. Assets are typically tallied as positives (+) in a balance sheet and broken down into two further categories: current assets and noncurrent assets.

Current assets typically include anything a company expects it will convert into cash within a year, such as:

- Cash and cash equivalents

- Prepaid expenses

- Inventory

- Marketable securities

- Accounts receivable

How to read a balance sheet Noncurrent assets section typically include long-term investments that aren’t expected to be converted into cash in the short term, such as:

- Land

- Patents

- Trademarks

- Brands

- Goodwill

- Intellectual property

- Equipment used to produce goods or perform services

Because companies invest in assets to fulfill their mission, you must develop an intuitive understanding of what they are. Without this knowledge, it can be challenging to understand the balance sheet and other financial documents that speak to a company’s health.

- Liabilities

Liability is the opposite of an asset. While an asset is something a company owns, a liability is something it owes. Liabilities are financial and legal obligations to pay an amount of money to a debtor, which is why they’re typically tallied as negatives (-) in a balance sheet.

Just as assets are categorized as current or noncurrent, liabilities are categorized as current liabilities or noncurrent liabilities.

Current liabilities typically refer to any liability due to the debtor within one year, which may include:

- Payroll expenses

- Rent payments

- Utility payments

- Debt financing

- Accounts payable

- Other accrued expenses

How to read a balance sheet Noncurrent section of liabilities typically refers to any long-term obligations or debts which will not be due within one year, which might include:

- Leases

- Loans

- Bonds payable

- Provisions for pensions

- Deferred tax liabilities

Liabilities may also include an obligation to provide goods or services in the future.

- Owners’ Equity

How to read a balance sheet Owners’ equity section, also known as shareholders’ equity, typically refers to anything that belongs to the owners of a business after any liabilities are accounted for.

If you were to add up all of the resources a business owns (the assets) and subtract all of the claims from third parties (the liabilities), the residual leftover is the owners’ equity.

Owners’ equity typically includes two key elements. The first is money, which is contributed to the business in the form of an investment in exchange for some degree of ownership (typically represented by shares). The second is earnings that the company generates over time and retains.

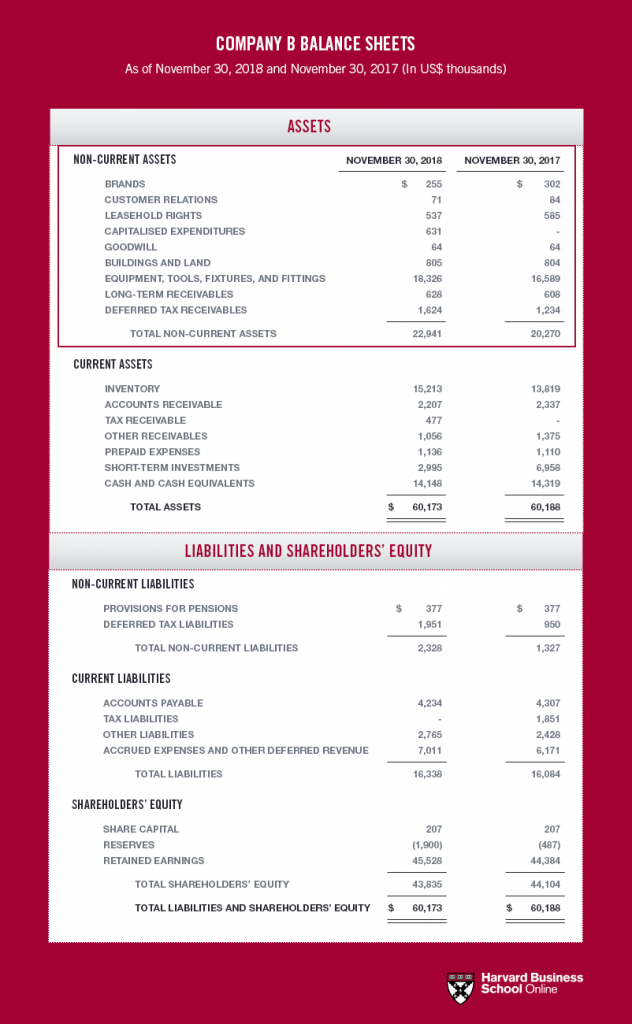

A BALANCE SHEET EXAMPLE

By looking at the sample balance sheet above, you can extract vital information about the health of the company being reported on.

For example, this balance sheet tells you:

- The reporting period ends November 30, 2018, and compares against a similar reporting period from the year prior

- The company’s assets total $60,173, including $37,232 in current assets and $22,941 in noncurrent assets

- The company’s liabilities total $16,338, including $14,010 in current liabilities and $2,328 in noncurrent liabilities

- The company retained $45,528 in earnings during the reporting period, slightly more than the same period a year prior

A CRUCIAL UNDERSTANDING

How to read a balance sheet information found in a company’s balance sheet is among some of the most important for a small business tax accountants to offer business leader advice, regulator, IRS or potential investor to understand. Without this knowledge, it can be challenging to know whether a company is struggling or thriving, highlighting why learning how to read and understand a balance sheet is a crucial skill for anyone interested in business. All the best accountants in Miami will advise their clients on the same key metrics.

How to Read a Balance Sheet

Welcome to the Gutenberg Editor

The goal of this new editor is to make adding rich content to WordPress simple and enjoyable. This whole post is composed of pieces of content—somewhat similar to LEGO bricks—that you can move around and interact with. Move your cursor around and you’ll notice the different blocks light up with outlines and arrows. Press the

How to Increase Profit Margins Through Virtual CFO Services

How to Increase Profit Margins Through Virtual CFO Services

Great Accounting Firms Share These 10 Traits

Great Accounting Firms Share These 10 Traits which has gone far beyond the paper-pushing days and now involves acting as a virtual CFO

Tax Accountant in Miami Cope with IRS Tax Season Delay

Tax Accountant said IRS delays start of tax season for individual returns would be postponed until February 17 with some as late as March

Miami Accountants Philosophy of Up or Out

Its up or out for Miami Accountants firms are faced with the dilemma of keeping long-term managers that are not ready to be equity partners or let them go.

Contadores en Miami Explican Auditorías del IRS

Contadores en Miami, Gustavo A Viera CPA, explica los pasos de una auditoría, desde la notificación de la auditoría hasta el cierre de la misma

Home » Blog » Accounting and tax » How to read a Balance Sheet